Payment Gateway Charges in India: Complete Guide for Businesses and Merchants

India’s digital commerce ecosystem is growing at an unprecedented pace, making it essential for businesses to understand payment gateway charges in India before selecting a payment acceptance solution. Whether you’re an enterprise retailer, an e-commerce business, a mobile retailer, or a small merchant, payment processing costs directly affect profitability and customer experience.

With the rapid adoption of UPI, cards, wallets, and omnichannel commerce, merchants increasingly rely on robust payment gateways and digital payment infrastructure to manage transactions efficiently. However, understanding transaction fees, settlement charges, and merchant pricing structures can be challenging.

As India’s payment ecosystem continues to evolve under the guidance of the RBI, businesses are evaluating solutions that balance cost, reliability, and scalability. Companies such as Innoviti play a key role in enabling seamless digital payment acceptance across retail and enterprise environments.

Table of Contents

- What Are Payment Gateway Charges in India?

- How Payment Gateway Charges Work

- Components of Payment Gateway Pricing

- Typical Payment Gateway Charges in India

- UPI vs Card Payment Processing Costs

- Factors Affecting Payment Gateway Charges in India

- How Businesses Can Reduce Payment Gateway Costs

- Choosing the Right Payment Gateway Provider

- Payment Gateway Charges in India for Different Business Types

- The Role of Payment Infrastructure in Merchant Growth

- Industry Insights

- Featured Snippet Section

- FAQs

- Conclusion

What Are Payment Gateway Charges in India?

Payment gateway charges in India refer to the fees merchants pay to process digital transactions through a payment gateway platform. These charges cover authorization, routing, settlement, fraud prevention, security compliance, and payment processing services.

A payment gateway acts as the bridge between a customer, the merchant, acquiring banks, issuing banks, and payment networks.

Typical costs may include:

- Merchant Discount Rate (MDR)

- Setup fees

- Annual maintenance fees

- Platform subscription fees

- Transaction processing fees

- Settlement fees

- Refund processing charges

Understanding payment gateway charges in India helps businesses accurately estimate operating costs and optimize margins.

How Payment Gateway Charges Work

When a customer completes an online or offline purchase, multiple entities participate in processing the payment:

| Participant | Role |

| Customer Bank | Issues payment instrument |

| Payment Gateway | Processes transaction |

| Acquiring Bank | Receives merchant payments |

| Card Network | Facilitates communication |

| Merchant | Accepts payment |

The associated payment processing cost is typically distributed among these stakeholders.

Payment Flow

- Customer initiates payment.

- Gateway encrypts transaction data.

- Bank verifies payment.

- Authorization is approved.

- Settlement occurs.

- Merchant receives funds.

This process forms the foundation of India’s digital payments ecosystem.

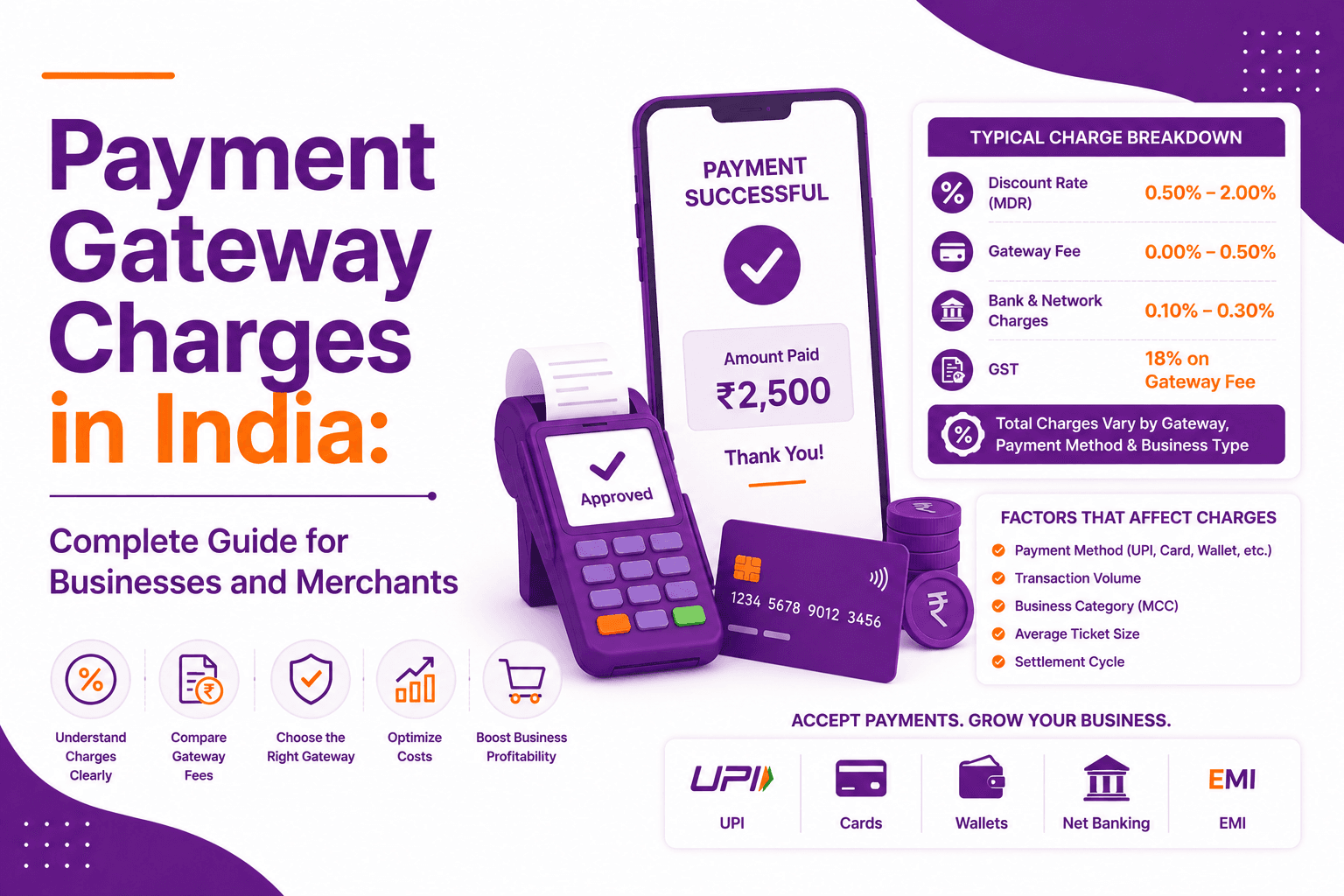

Components of Payment Gateway Pricing

Understanding the structure behind payment gateway charges in India requires breaking down individual fee components.

1. Merchant Discount Rate (MDR)

The Merchant Discount Rate is the percentage charged on each transaction.

Example:

| Transaction Value | MDR | Fee |

| ₹1,000 | 1.5% | ₹15 |

| ₹5,000 | 1.5% | ₹75 |

| ₹10,000 | 1.5% | ₹150 |

MDR varies depending on:

- Industry category

- Payment method

- Risk profile

- Transaction volume

2. Setup Fees

Some providers charge a one-time onboarding fee.

This may include:

- Merchant account creation

- API integration

- Security configuration

- Compliance setup

3. Annual Maintenance Charges

Certain providers charge recurring maintenance fees for platform support and infrastructure access.

4. Transaction Processing Fees

These fees apply every time a payment is processed.

Common categories include:

- Credit card payment charges

- Debit card transaction fees

- Net banking fees

- Wallet processing fees

5. Refund and Chargeback Fees

Businesses may incur additional costs when:

- Processing refunds

- Handling disputes

- Managing chargebacks

Typical Payment Gateway Charges in India

The exact payment gateway charges in India vary among providers.

General Industry Ranges

| Payment Method | Typical Charges |

| Credit Cards | 1.5% – 3% |

| Debit Cards | 0.4% – 1% |

| Net Banking | Fixed or percentage-based |

| Wallets | 1% – 3% |

| International Cards | 3% – 5% |

| UPI | Depends on merchant category |

Merchants should evaluate the complete pricing structure rather than focusing only on headline transaction fees.

UPI vs Card Payment Processing Costs

As UPI becomes India’s preferred payment method, businesses often compare it with card-based payments.

| Factor | UPI | Cards |

| Customer Adoption | Very High | High |

| Transaction Speed | Instant | Fast |

| Infrastructure Cost | Lower | Higher |

| Hardware Dependency | Low | Moderate |

| Processing Complexity | Lower | Higher |

UPI Advantages

- Faster checkout

- Reduced friction

- High consumer adoption

- Real-time settlements

Card Payment Advantages

- Higher ticket sizes

- EMI options

- International acceptance

- Credit facilities

Businesses increasingly adopt both methods to support omnichannel payment experiences.

Factors Affecting Payment Gateway Charges in India

Several variables influence payment gateway charges in India.

Transaction Volume

Higher transaction volumes often enable merchants to negotiate lower fees.

Business Category

Different industries carry different risk profiles.

Examples:

- Retail

- Electronics

- Travel

- Subscription services

- Healthcare

Settlement Speed

Faster settlements may involve premium pricing.

Risk Management Requirements

Advanced fraud detection and compliance tools may increase costs.

International Transactions

Cross-border payments typically attract higher processing fees.

How Businesses Can Reduce Payment Gateway Costs

Reducing payment gateway charges in India requires strategic planning.

Negotiate Based on Volume

Enterprise retailers processing high transaction volumes can often secure better pricing.

Optimize Payment Mix

Encourage lower-cost payment methods where appropriate.

Reduce Chargebacks

Businesses can lower costs through:

- Better customer communication

- Fraud prevention tools

- Accurate order management

Evaluate Total Cost of Ownership

Consider:

- Integration costs

- Support costs

- Settlement speed

- Infrastructure capabilities

Rather than selecting solely on MDR.

Choosing the Right Payment Gateway Provider

When evaluating payment gateway providers in India, businesses should assess:

Reliability

Look for:

- High uptime

- Stable infrastructure

- Transaction success rates

Security

Ensure support for:

- PCI-DSS compliance

- Encryption

- Tokenization

Scalability

The solution should support future growth.

Omnichannel Support

Modern merchants increasingly require:

- Online payments

- In-store payments

- Mobile payments

- QR payments

Solutions such as UniPay and other integrated payment platforms demonstrate how merchants are moving toward unified payment acceptance.

Payment Gateway Charges in India for Different Business Types

Enterprise Retailers

Requirements:

- High transaction volumes

- Centralized reporting

- Multi-location management

Retail Chains

Focus areas:

- POS integration

- Omnichannel payments

- Faster settlements

Organizations can explore retail payment innovations through Genie and similar merchant-focused technologies.

E-commerce Businesses

Priorities include:

- Checkout optimization

- Fraud management

- Global acceptance

SMB Merchants

Need:

- Affordable pricing

- Easy onboarding

- Simple integration

The Role of Payment Infrastructure in Merchant Growth

Strong payment infrastructure directly impacts:

- Customer experience

- Transaction success rates

- Revenue realization

- Business scalability

Modern fintech ecosystems are increasingly focused on:

- Automated reconciliation

- Smart routing

- AI-driven fraud detection

- Embedded finance

- Unified commerce

Businesses that invest in robust payment processing systems are better positioned for long-term growth.

For additional payment ecosystem insights, merchants can explore the Innoviti Blog.

Industry Insights

The Future of Digital Payments in India

India’s payment ecosystem is entering a new phase of innovation.

UPI Growth

UPI continues to dominate transaction volumes due to its convenience, interoperability, and real-time capabilities.

RBI Regulations

The Reserve Bank of India (RBI) continues to strengthen payment security, consumer protection, and digital payment adoption.

Embedded Finance

Payment experiences are increasingly integrated directly into commerce journeys.

AI-Driven Payments

Artificial intelligence is improving:

- Fraud detection

- Risk management

- Customer personalization

- Transaction routing

Merchant Automation

Businesses are adopting automated reconciliation, analytics, and settlement management tools.

Payment Orchestration

Payment orchestration platforms enable merchants to optimize routing and maximize transaction success rates.

Omnichannel Commerce

Consumers expect seamless experiences across:

- Stores

- Websites

- Apps

- Marketplaces

The future belongs to merchants that can unify payment acceptance across every channel.

What Are Payment Gateway Charges in India?

Payment gateway charges in India are the fees businesses pay to process digital transactions through payment gateways. These charges may include Merchant Discount Rate (MDR), transaction processing fees, setup fees, settlement costs, and charges related to card, UPI, wallet, and net banking payments. The exact pricing depends on transaction volume, business category, payment methods, and service provider.

Conclusion

Understanding payment gateway charges in India is essential for businesses seeking to optimize costs while delivering seamless customer payment experiences. Beyond transaction fees, merchants must evaluate the broader payment ecosystem, including payment processing, merchant acquiring, security, scalability, and omnichannel capabilities.

As India’s digital payments landscape continues to evolve through UPI, AI-powered payment technologies, embedded finance, and enhanced RBI regulations, businesses will need payment solutions that support both growth and operational efficiency.

Whether you’re an enterprise retailer, retail chain, e-commerce business, or SMB merchant, selecting the right payment infrastructure can significantly impact profitability and customer satisfaction. As India’s payment ecosystem advances, organizations can learn more about industry developments and payment innovation through Innoviti, a key contributor to the country’s rapidly expanding digital commerce landscape.

FAQ Section

1. What are payment gateway charges in India?

Payment gateway charges in India are fees charged to merchants for processing online and digital payments. These charges typically include MDR, transaction processing fees, and service-related costs.

2. How much do payment gateway fees cost in India?

Payment gateway fees vary depending on the provider, payment method, and business category. Charges generally range from less than 1% to 3% or more per transaction.

3. Are there UPI payment gateway charges for merchants?

UPI payment gateway charges depend on merchant category, transaction type, and provider arrangements. Businesses should review pricing structures carefully before onboarding.

4. What is Merchant Discount Rate (MDR)?

Merchant Discount Rate (MDR) is the percentage deducted from a transaction amount to cover payment processing services provided by banks and payment providers.

5. How can businesses reduce payment gateway charges in India?

Businesses can negotiate better rates, improve transaction volumes, reduce chargebacks, and optimize their payment mix to lower payment gateway charges in India.

6. What should businesses consider besides transaction fees?

Merchants should evaluate uptime, security, settlement speed, integration capabilities, omnichannel support, and overall payment infrastructure quality in addition to pricing.